The Fed Goes Meta

December Recap and January Outlook

While the equity markets, as measured by the S&P 500 index, was up in the third quarter, December was a disappointment from the gains seen in October and November. For context, Dow Jones Market Data indicates that the S&P saw more market moves of 2% (both up and down) in 2022 than in 2020. The 46 moves over the 2% threshold are approximately four times the 10-year average of 11.3.

Inflation is dropping, if slowly. Employment is lower, but strong, which is supportive of the economy, and GDP returned to positive. What’s causing the volatility? Many factors are in play, but arguably the largest is the Federal Reserve’s moves on interest rates, and the messaging from Chairman Powell and the Fed Governors.

Let’s get into the data:

- 12-month CPI was 7.1% in November. The Bureau of Labor Statistics reported number was lower than expectations

- The December non-farm payroll number was 223,000. The report from the Department of Labor was a decrease from the November number, and slightly above expectations

- The unemployment number edged back down to 3.5%. This statistically matched the lowest number since 1969

- Three-month wage growth averaged 4.1%. The number includes revisions to prior months. This compares favorably to the 5.8% growth seen before revisions and seems to indicating a more normal rate.

What Does All of That Data Add Up To?

While an overstatement, it does seem at times that the only data the market is interested in are the number of hundredths of a percentage point of that make up the increase in the Fed Funds rate – and when that will go to zero or turn into a decrease.

No one seems more aware of this than the Fed. Back in the day, before 2008, pronouncements from the Federal Reserve were crafted to be obscure so as to avoid moving markets. This changed over time and with successive Fed Chairmen to a more direct approach. The current Chairman, Jerome Powell, has evolved still further. First, we had the “Fed ratchet” of earlier this year, in which Powell telegraphed moves that the market could adjust to gradually.

This may have worked too well. While asset values have declined, the market remains poised to bounce up at every hint that the Fed may slow or stop rate increases. This may be masking or even delaying the impact of rate increases in slowing the economy and bringing inflation down.

With the economy seeing a lagging impact from rate increases already enacted, this is complicating the Fed’s ability to accurately read the economic tea leaves and know when to stop in order to avoid a recession.

Powell has resorted to using the Fed’s pronouncements to continue to assert that bringing down inflation is the highest priority and that any thought that the Fed will ease off before the job is done is a “misperception.” This could be read as an attempt to influence the market and keep asset values lower.

Whether the resolve is solid remains to be seen. While Powell is clear on getting inflation down, the Fed is still positioning a “soft landing” in which the economy avoids recession as a possibility. That would require some easing of rates.

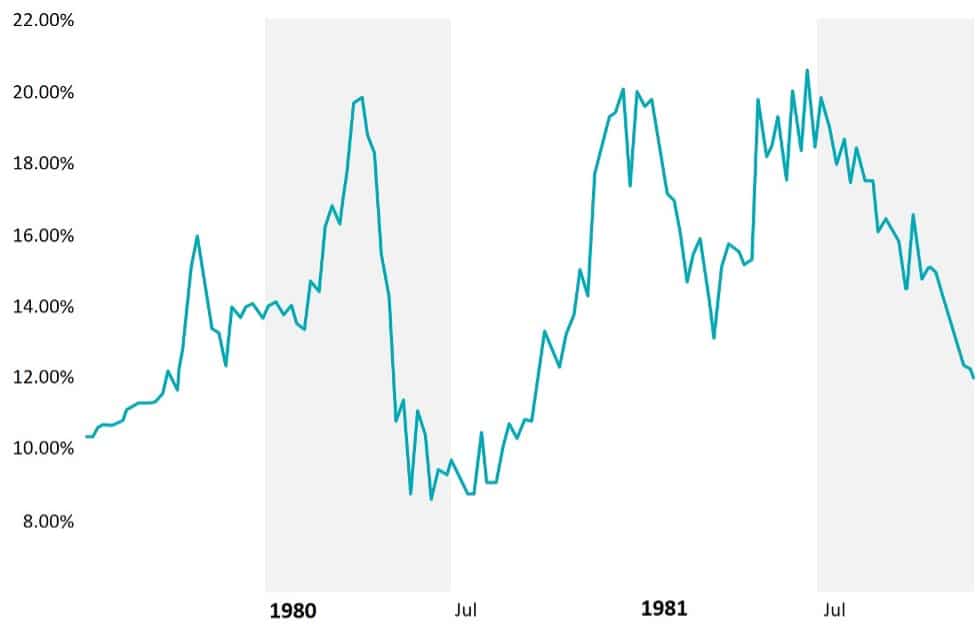

Chart of the Month: Fed Funds Rate, early 1980s

The chart below tracks the path of the Fed Funds rate between July 1979 and November 1981. This whipsaw is exactly what the Fed is trying to avoid. A recession in early 1980 (indicated by the shaded area on the chart) resulted in a massive decrease to the Fed Funds rate – which was followed by an increase and another, longer recession.

Source: Macrotrends.net, Fed Funds Rate 62-year Historical Daily Level

Equity Markets in December

- The S&P 500 was down 5.90% and finished the year at -19.44%

- The Dow Jones Industrial Average lost 4.17% and had a year end result of -8.78%

- The S&P Mid-Cap 400 returned -5.72% and full-year performance was -14.48%

- The S&P Small-Cap 600 decreased 6.89% and was down 17.42% for the full year

Source: S&P. All performance as of December 30, 2022

December reversed the positive performance of October and November, and despite a small “Santa Claus” rally, all 11 sectors declined. Utilities saw the smallest decline of 0.77%, and Consumer Discretionary saw a whopping 11.31% decrease for the month. 2022, Energy was the only positive sector for all of 2022, up 59.04%, and Communication Services was the worst sector, down 40.42%.

Bond Markets

The 10-year U.S. Treasury ended the month at a yield of 3.88%, an increase from 3.61% in November. For comparison, the 10-year yield was 1.51% at year-end 2021. The 30-year U.S. Treasury ended December at 3.97%, up from 3.75% last month. The Bloomberg U.S. Aggregate Bond Index ended December with a return of -0.45%. The year-to-date return at month end was -13.01%, continuing the trend positive correlation between the equity and bond markets.

The Smart Investor

The ongoing strength of the labor market is providing some hope that if 2023 does see a recession, it will be mild. However, predictions are that growth will slow from its already low levels. The path of the markets is likely to be as choppy as 2022, with observers and investors still playing “watch the Fed” and the Fed attempting to fight inflation while managing expectations in a way that will be helpful to Fed policy and not fight it.

What should investors focus on? The same thing as every year: your own goals. There’s no substitute for having a plan, no matter what stage you are in. The SECURE 2.0 act has made meaningful improvements to the ability of just about everyone to save for retirement, or conserve retirement savings. Updating your plan to take advantage of the new opportunities makes sense.

There are some tactical things you may want to think about:

- 401(k) limits increased. Think through when you’ll contribute. If you normally use a bonus for this, you may want to consider a different approach

- The age for required mandatory distributions increased – consider taking advantage of the additional year to lower account values through a Roth conversion

- Don’t forget your RMD, or complete a qualified charitable distribution to offset it

- Ongoing volatility means diversification is even more important

The start of the year is all about resolutions. But there’s a reason that the second Friday of January is known as “Quitter’s Day.” When it comes to your financial plan, having resources build and monitor an ongoing structure that runs in the background and help you achieve your goals.

IMPORTANT DISCLOSURES

Advisory services are offered through TCG Advisors, an SEC Registered Investment Advisor. Insurance services are offered through HUB International. TCG Advisors is a HUB International company.

Note: This message is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security, or as an offer to provide advisory or other services in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. Remember all investing involves risk.

Part of this material was prepared by Broadridge Investor Communication Solutions, Inc. and powered by Advisor I/O under the Terms of Service. Although the information in this blog has been compiled from data considered to be reliable, the information is unaudited and is not independently verified. TCG.4.2023

Financial assistance is available! Get matched with a Financial Advisor: